Mining in Ghana: A long & twisted tale of disappointment

Civil Society advocates active in the natural resources policy space in Ghana have been left disappointed by the failure of imagination among politicians and senior civil servants negotiating Ghana’s first lithium mining lease.

It is safe to say that almost no Ghanaian is happy about the historical and contemporary reality of mining’s contribution to the country. For a country that has a 500-year reputation for being a haven of gold (with large-scale commercial gold mining dating from at least 1897), was once the 5th largest producer of the metal, and currently the largest in Africa, many Ghanaians look around them and frown when they don’t see the glamour of Johannesburg’s Sandton.

The Manic Past of Lithium

News that Ghana had signed a mining lease with an Australian junior miner to produce lithium from 2025 therefore raised hackles. Coming just weeks before the COP28 Summit in Dubai, with all the razzmatazz around green energy and the “climate transition“, the question on every Ghanaian’s lips was: “would lithium be the gamechanger when oil and gold appear to have disappointed”?

Answering that question, especially in relation to the agreement Ghana has just signed, requires a bit of a detour to explore why such hype has been building around lithium in the first place.

Highly reactive and inflammable, lithium, the lightest metal on Earth, now affectionately referred to as “white gold”, was first detected as a trace element in 1817 and isolated in 1855. For decades thereafter, its renown was gained by its use by some physicians in the management of mania, depression and bipolar disorders more generally. Hardly surprising then that it is inducing such frenzied mania today.

The Lithium Rush

As the 20th century proceeded, lithium began to find more applications across areas such as ceramics, glassware, polymers, castings, medicines (of course), and others. A few years ago, however, one use of lithium has far exceeded all others: batteries to power the electric vehicle (EV) boom. Today, more than 85% of all lithium demand is for use in lithium-ion batteries.

Some analysts believe that by 2050, lithium would have seen the fastest growth among all the minerals usually associated with the green transition.

Lithium chemistry can confuse you

Because lithium is such a reactive element, unlike, say, gold and aluminum, which are considered “inert” (relatively so in the case of the latter), its economic importance is often expressed through a bewildering array of intermediate and end-state compounds, such as lithium hydrochloride, lithium carbonate, and, to a much lesser extent, lithium bromide.

Therefore, when discussing lithium economics, one should always be very clear about which chemistries, chemical pathways, and compounds and salts are involved. Much depends on how lithium combines with other substances, either naturally or during processing, to arrive at a particular economic use case.

For example, during the recent bull era, when lithium prices exploded, the margin on refining the concentrates of spodumene, the most common rock ore of lithium, into lithium hydroxide, one of the compounds that in its most refined state goes into batteries, was about 35%.

Depending on the relative inventory levels of spodumene concentrate and lithium hydroxide in dominant markets like China, that margin can fluctuate much more crazily than is the case in some value chains we are more familiar with like cocoa, gold and bauxite. Again, this calls for smart economic contracts that are somewhat flexible enough to ride the storms.

The Economics of Ghana’s lithium deal draws scrutiny

Given this context, civil society analysts in Ghana have been painstakingly poring over the Definitive Feasibility Study (DFS) submitted in the disclosures of Atlantic Lithium, the company recently granted Ghana’s first lithium mining lease (subject to parliamentary ratification), to the alternative submarket of the London Stock Exchange (and concurrently to the Australian Securities Exchange, where it is also listed). The reader may find the highlights below.

The easiest observation to make from the DFS is that the proposed lithium operations are juicily profitable. For the company. With a post-tax margin of roughly 23%, and relatively low capex (revised a number of times to about $195 million), investors look to be sitting pretty. Due to Atlantic Lithium’s relatively conservative posture in the DFS at the height of the lithium boom, its numbers are only looking a bit off (the projected price of its highest grade concentrate – SC6 – for instance has had to be revised downwards from $1695 to $1410 per tonne according to recent statements by Ghana’s mineral authorities).

What civil society observers are asking is whether the Ghanaian people, by law the ultimate owners of the resource, would be just as comfortable over the 12-year course of mining of these deposits in the Ewoyaa region of the country’s central coast. We will come to that shortly.

Putting Ewoyaa in context

Zimbabwe is Africa’s largest producer of lithium. It is believed to hold the world’s fifth or sixth largest reserves of the metal. Yet, the country is on course to make just about $250 million from the mineral this year, out of total mineral earnings of about $5.67 billion (2022).

Bear in mind that Ghana, in a good year, can generate more than $6.6 billion from gold exports (how much of that actually stays within the economy is a different matter). Despite all the hubbub about Africa’s lithium, the continent currently holds only about 5% of the world’s known reserves. All this to say that the lithium game is just beginning. Any premature excitement is likely to be, well, premature.

Lithium does deserve special attention

The above notwithstanding, there are interesting aspects of the lithium value chain that requires that countries not take a business as usual approach. Compared to, say, cocoa, where the cocoa beans often struggle to capture even 3% of the value of marketed outputs, things can be different in the case of lithium.

Provided one refines lithium into the form, such as lithium carbonate or hydroxide, that can be used in battery components like the cathode, one can capture 30% of the value of the battery. Compare that to, say, cocoa powder, where there have been years in which margins have been actually negative (i.e. producing cocoa powder makes less money than leaving the cocoa in beans form).

These value chain margin analytics are further compounded, as hinted earlier, by the fact that valuable lithium end-products like batteries often require other green minerals to make, interlinking the economics of lithium with that of various strategic complements. Below, the reader may scan a number of battery technologies and notice two things: the involvement of other green minerals besides lithium and the tendency of major buyers of lithium end-products like batteries to make a strategic commitment to one combination/configuration of green minerals or the other.

With that highly condensed crash course out of the way, we can begin a discussion about Ghana’s contract with Atlantic Lithium and start to shed light on why some in Ghanaian civil society believe that government Ministers and the officials advising them are being too self-congratulatory.

How Unprecedentedly beneficial was the lithium deal?

First, the money (see key terms in the snapshots below). The government’s big case is that it has secured concessions from Atlantic Lithium that no government has been able to obtain in the country’s history. If this is based purely on how the gains from the resource are to be shared between the government and the investor, in ownership and monetary terms, then that fact is simply incorrect.

It is common knowledge in Ghanaian natural resource settings that the share to the state of resource gains was heftier in the 1970s and the early 1980s, and even after reforms came in the late 1980s, those terms were generally more favourable than what ensued in the subsequent decades.

In the 1970s, the Ghanaian government introduced policy to set a floor of 55% under the ownership stake of the state in producing mining concessions. In recent comments, the Chief Executive of the Minerals Commission has sought to imply that this history does not count because it encompasses a period of wholesale nationalisation. Fact is, that is simply incorrect.

While one effect of the Mining Operations (Government Participation) Decree of 1972 was the complete nationalisation of some mines, such as the African Manganese Company, some of the privately controlled mines were not nationalised per se. The policy simply led to a government majority of the equity stake in previously privately-held mining firms. However, in virtually all cases, the state’s equity participation went up to 55%, except for those mines it outrightly owned.

As eminent Ghanaian jurists, S.K.B Asante and S.K. Date-Bah have carefully chronicled in their work on joint ventures in the Ghanaian mining industry, the Ghanaian government negotiated an equity stake of 20% in Ashanti Gold Corporation in 1969. How can a negotiated outcome be considered “nationalisation”? After the negotiated joint venture between the government of Ghana and Lornho, the parties went further to negotiate an option for the state to acquire a further 20% in the future if it chose to do so. The government was also given the right to appoint four board members. Even this agreement was highly criticised by experts at the time due to the insufficient care paid to all the tax implications.

It is important to bear in mind that the action of the succeeding Acheampong government to ensure government majority in the mining companies was based on a policy paper published in December 1972. The prescriptions of this paper were to be translated into action by an interdisciplinary committee of experts, drawn from across the different professional strands of society. It was chaired by Dr. S.K.B. Asante. This team went to London to negotiate with Ashanti Gold in respect of the government’s desire to increase its stake. The passing of the decree was part of the negotiating tactics adopted by the government to strengthen the hands of the committee. Below, the principal terms of the final agreement are reproduced by the two aforementioned jurists.

In substance, therefore, if we are to limit ourselves purely to the split of gains between the government and the private investor, then both the purely negotiated 1969 Ghana – Ashanti Gold agreement and the, decree-backed, 1972 agreements between the same parties were better than the recent lithium deal by having offered the State 20% and 55% (compared to the 13% in the lithium deal), respectively, of the total equity in the concession.

Likewise, the various joint ventures that the government continued to enter into following the reforms of the late 1980s saw government take up large equity positions, as was the case in the Konongo Gold Project, where Southern Cross Mining held 70% and the state, 30%.

On the issue of royalties, comparison with historic episodes is fraught with confusion because in the past Ghana had a variable rate margin that could take the due royalty entitlement to more than 10%. The 1987 regulations passed during the reform era when Ghana sought to increase private participation in mining again constitute one clear example in this regard.

Confining ourselves to the narrow dimension the government of Ghana itself has selected, we can boldly assert that the claim that the terms of the recent lithium deal are the “best” in Ghana’s history is factually inaccurate. It is important that senior civil servants of such high stature strive for objectivity in their public communications.

Another argument canvassed by the Chief Executive of the Minerals Commission is that despite the existence of the variable royalty structures in various contracts historically, and despite his acknowledgement that this could lead to the royalty rate exceeding 10% in these contracts, those terms were in the end meaningless because no mining investor ever paid a royalty rate above 3% (until the Finance Minister in the Mills government initiated a change in royalty rate to 5%). Once again, this claim is contentious, considering the span of mining history in Ghana and the very patent record of joint ventures paying the variable rate based on operating margin. Even in more recent years, we have had companies pay above the royalty treshold, as was the case of the operators of the Chirano mine in 2017.

At any rate, as the AfDB has noted, the failure of the variable tax regime to hit the higher threshold levels is primarily due to the exploitation of loopholes. If duty-bearers and office-holders continue to underperform in their functions, then the history of failure we have witnessed will be due less to the absolute terms found in the various agreements and more to their implementation and enforcement.

To sum up this section, taking the country’s full span of history into account, the lithium deal is not exceptional.

Paperwork is not enough

The heart of the matter though is that nice fiscal terms on paper, however “generous” to Ghana, however “resource nationalistic”, would not mean much if overall management of the sector and/or the investment climate is bad. Contracts and leases should thus be designed in such a manner that they will prove resilient even in the face of weak regulatory performance.

That is why the period when Ghana saw the most nationalistic contracts in the 1970s and 1980s was also the period when it lost its leadership in the African mining sector. Over the course of that era, Ghana’s active gold mines declined from about 34 to just 4. Mismanagement, weak technical capacity, poor investment policies, and a host of factors conspired to prevent the intent of higher social returns to mining from materialising.

Hence why fiscal regimes are hard to compare across countries

Whilst the effort at benchmarking should be highly commended, the government’s selective use of comparative data across African countries to elevate the success of the lithium deal is not as compelling as it could be because it strips some of the numbers of context, uses outdated data, and fails to include instances that are not as favourable for the goals of the comparisons.

For example, it rightly mentions Namibia as a country where the government is not entitled to a free, mandatory, equity stake in mining concessions it gives out. But it does not mention the higher income tax bracket for mining. The infographic above issued by the government states the wrong upper bound for Chile’s royalty structure, which is 40% instead of 26%. There is no acknowledgement of the radical public-private partnership arrangements now in place in both Chile and Mexico, and which effectively make lithium an extension of national security policy. Zimbabwe’s fiscal terms are described without regard for the fact that it also has concessions where state actors are directly involved in the actual mining. Mali is mentioned as limiting itself to a 10% free/carried interest without regard to recent announcements that the state will now be able to increase overall participation (both free and fair-market acquisitions) to 30%.

Instead, the Chief Executive of the Minerals Commission spent time quibbling with this author whether Zimbabwe’s new law restricting unbeneficiated exports cover concentrates, even when the definition in the law explicitly mentions concentrates, tailings, slag, slime etc. And when that point was totally irrelevant to the central point about differentiated strategies across countries requiring a more in-depth analysis than just posting headline figures, including incorrect figures.

Sophistication is required

All the aforementioned complexities make it clear that much sophistication is required in the design of the legal technologies used in contracts in the emerging lithium era.

For example, Ghana’s royalty rate is tied to the sales price achieved through the concessionaire’s own arrangements alone.

Unlike India’s regime where an independent price benchmark is used (LME). In a situation where more than half of the lithium mine’s output is destined to be sold to related parties in potentially non arms-length transactions, one worries whether the government should not have explored a pricing index in the agreement.

Real Options are a must for fast-changing markets like lithium

Atlantic Lithium’s offtake agreements and customer-financing strategies reflect the fast changing dynamics in the green economy as companies and governments jostle to position themselves ambidextrously lest they be outmaneuvered by trends.

“Real options” is a field of finance designed specifically to handle such situations. The concept represents an array of “strategic choices” the government of Ghana could have reserved in the contract with Atlantic Lithium without overencumbering itself with obligations.

One of the uncertainties in the lithium market that strongly advise the use of real options include the fast changing terrain of new battery technologies. It is not far-fetched at all to envisage a future, not too far away, in which lithium-ion batteries become obsolete and are replaced by some liquid-free selenium derivative or another non-lithium option in the table below.

Another technological trend to watch closely is the pace at which lithium battery recycling is maturing. A time may come when demand for primary-mined lithium goes down significantly because so much is being produced from recycling old batteries.

Besides technological shifts is the ongoing price volatility that has seen prices of lithium compounds tumble of late. At the peak of the bull run, in November 2022, lithium hydroxide prices hit a high of $81,000 per tonne only to plunge to $16,500. A fate that did not befall some competing and complementary green metals.

Yet more reasons for tighter structuring and creative options

On top of all the above is the obvious fact that Ghana’s lithium prospects have been placed in the hands of a small junior miner with very limited experience. Some of our oil field woes have been blamed on a similar tango with junior producers.

Atlantic Lithium, the only lithium lease-holder in Ghana, is so small that to raise $13.2 million on the stock market in mid-2022, it had to make up mining rights it didn’t then have.

Its complicated structure and multiple leases (for its size and scale) in Ghana also makes it quite difficult for the independent analyst to fully understand the valuation structures at play.

Ghana’s Sovereign Fund goes gaga with joy

Which all makes it curious to see how Ghana’s Sovereign Wealth Fund has been celebrating its “wins” following the agreement to buy into the Ewoyaa project and the Atlantic Lithium holding structure itself.

So enthusiastic was MIIF that it does not even seem, from all the information it has put out, to have negotiated any anti-dilution provisions, knowing very well that given its very early stage of operations, the likelihood of serious dilution of its stake is very possible.

MIIF has in the last couple of weeks put out various statements celebrating “capital gains” that it says it has already made from its planned investment in Atlantic Lithium.

The claimed “capital gains” appear to have been computed from a short trading run without regard to the volatility of the stock. MIIF bought at 26 US cents a share and plans to buy more in the future at 36 US cents. But Atlantic Lithium’s share price yesterday closed at just a little above 27 US cents, and could fall further if lithium prices continue their downward slide. Everyone, including the cleaner at MIIF, knows full well that it is much too early to announce capital gains on an asset that is even yet to reach financial close.

Even more curiously, MIIF has given two distinct valuations for the Ewoyaa project in a short interval using two very different methodologies, seemly unmindful of how the massive discrepancy will raise eyebrows. In one statement, it claims the Ewoyaa asset is worth $1.4 billion, and in another that is more like $691 million. Did the asset lose more than $700 million of its value already?

At any rate, Piedmont, which has been the primary financier of the Ewoyaa exploratory work that has led to the declaration of commerciality has provided some numbers that seem to place valuation at $360 million thereabouts, considerably lower than the MIIF estimates.

Back to the agreement itself. A careful reading of the text reveals a range of contingencies with no timelines or specific performance bounds.

When exactly should the scoping study for the chemical refinery (not the “side minerals” like kaolin and feldspar that the Chief Executive of the Minerals Commission has been talking about) be completed? The agreement doesn’t say. Yet, the provision is clear that unless the scoping study is satisfactory, Atlantic Lithium would have no obligation to build the refinery.

What does “outcome” in the above text mean? An after-tax IRR of 27.5%? 125%? 12.5%? There is simply nothing in the agreement to explain what exactly is the benchmark for feasibility in the proposed scoping study.

The same concern goes for the actual chemical refinement benchmarks. Nothing in the agreement confirms what particular chemistry end-states will be acceptable to the Republic of Ghana. Will refining 5.5% spodumene concentrate into 6% concentrate pass the test? What about producing lithium chlorides or sulphates, as intermediates for a desired end-state like carbonate or hydrochloride? What purity would satisfy Ghana? Must it be battery-grade? Clearly, some basic supplemental technical annexes would have helped in a situation like this? And even some scenario and sensitivity analysis?

Geopolitics & the Regional Dimension

The lack of a green mining law means that many references in the agreement to “legislation” refer to the same provisions in the general natural resources law that the government felt needed updating hence the dedicated green mining policy and the efforts to ensure that the lithium agreement is not business as usual.

The fact also that the Green Mining Policy on which the agreement was supposedly based was not subject to wide consultation in Ghana means that everyone is left guessing as to even the most rudimentary strategic considerations currently guiding Ghana’s goal of emerging as a lithium value addition hub.

Everyone knows that the Atlantic Lithium mining lease was framed in terms of a victory of the US against China since this is the first time an American company has secured access to a significant source of lithium from Africa to feed an American refinery (the Piedmont facility in Tennessee). Chinese investors, on the other hand, have won quite a number of these hits. Could Ghana have leveraged these geopolitical stakes to secure more involvement by American suppliers of complementary inputs and resources to make the path to value addition much clearer?

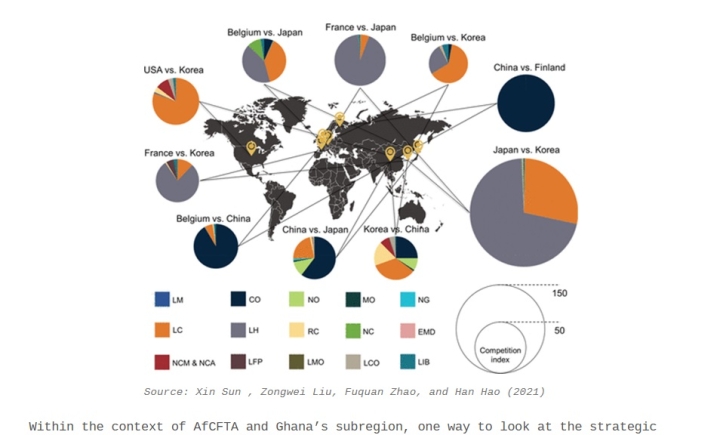

The fact that strategic complements and substitutes in the green energy value chain shapes the geopolitics of commodities like lithium is now very well appreciated. In an elaborate study by a group of Chinese academics at Tsinghua University, these strategic interplays were condensed into an index to simplify analysis of when cooperation works, and when competition dominates.

Within the context of AfCFTA and Ghana’s subregion, one way to look at the strategic complements dimension is to settle on a particular battery technology whose pursuit would catalyse regional and national value chains integration.

For example, making a strategic bet on lithium-iron-phosphate (LFP) would mean greater complementarity between the country’s stalled iron ore mining and nascent lithium mining ambitions, whilst creating room for greater engagement with Togo on phosphate trading since this West African neighbour currently limits its value addition strategy, where phosphate is concerned, to fertiliser.

The fact that LFP batteries are also increasingly winning on more dimensions against close competitor, Nickel-Manganese-Cobalt (NMC) batteries make such a gambit very interesting.

Of course, the presence of nickel and cobalt in other regions of Africa could mean that some NMC bets may work but the large distances on the continent counsel some conservatism in supporting a Ghanaian-Togolese integration.

A Chance to improve the actual licensing regime?

Lastly, the issue of whether Ghana could have done better if it had used more competitive methods to allocate lithium mining concessions has come up.

Officialdom have tried to dismiss this concern by claiming that tenders or auctions would not have been viable as Ghana does not have any geological data and therefore owes it to Atlantic Lithium’s data collection efforts to reward it with the mining lease. Such a lens is quite poor.

It presupposes that auctions cannot happen at prospecting level, before companies have spent money collecting investment-determining data. Ghanaian geologists have known, since at least 1916, about the presence of rock formations in the Cape Coast area featuring the kinds of pegmatites and lepidolites typically associated with lithium deposits. That is precisely why the likes of Atlantic Lithium and its previous incarnates knew where to concentrate their prospecting resources. In such circumstances, there is no reason why Ghana could not, and going forward cannot, use the auction method to attract more capable firms and begin to get a sense of which of them are most predisposed to providing favourable terms if prospecting is successful.

If this lithium situation has thought us anything at all, it is clearly that “good” may sometimes not be good enough. The government is to be commended for having the presence of mind to understand the citizenry’s demands for “better than usual”. It must now show readiness to deliver that “better” in this and upcoming mineral rights issues.

We call on the government to support Parliament in scrutinising the signed agreement with a fine comb and to stand ready to make the necessary amendments to the agreement terms to satisfy a country that has grown more alert, more impatient for “better”, and more sophisticated than politicians give it credit for.

Source: Bright Simons